Our company recognizes the critical importance of implementing different levels of Know Your Customer (KYC) procedures for different customers. By tailoring the KYC process to the specific risk profiles of each customer, we can effectively mitigate potential threats and ensure compliance with regulatory requirements. High-risk customers undergo a more rigorous and detailed KYC assessment, enabling us to identify and address any suspicious activities promptly. At the same time, low-risk customers experience a streamlined process, facilitating a seamless onboarding experience. Additionally, our company implements separate KYC procedures for individual customers and corporate entities, acknowledging the unique requirements and characteristics of each category. This approach allows us to maintain compliance and transparency while catering to the diverse needs of our valued clients.

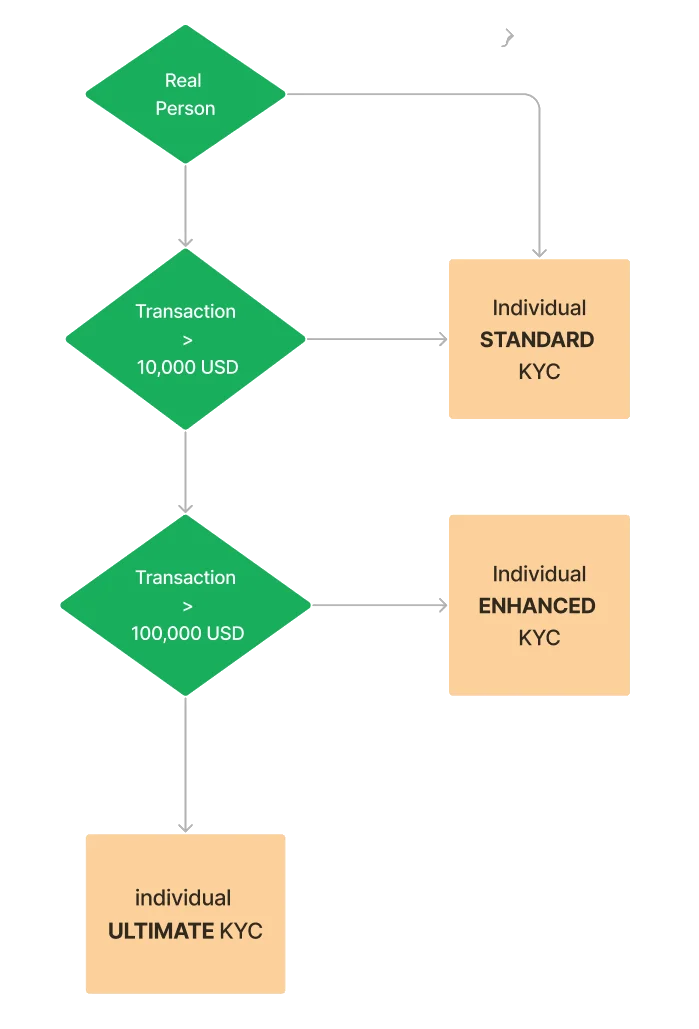

In the upcoming diagram, we illustrate the rationale guiding our decision-making process to determine the appropriate KYC level when dealing with a Real Person*

* an individual, not a corporate entity

The specifics of each KYC level provided below will provide a comprehensive understanding of our approach. These detailed descriptions will elucidate the varying requirements and scrutiny applied to individual customers, ensuring a robust and effective KYC framework.

Standard KYC – Individual

CryptoForce will establish and verify the identity of any counterparty with or for whom it acts or proposes to act. CryptoForce may update its counterparty identification policies, procedures, systems, and controls, considering its risk assessment related to the counterparty. The following list should be considered as guidance regarding the type of information and evidence that CryptoForce must obtain to establish and verify the identity of a counterparty before conducting any transactions or entering into any business relationships:

- Full name

- Date of birth

- Citizenship

- Current residential address

- Official I.D

- Source of funds

Enhanced KYC- Individual

We employ enhanced KYC measures when the transaction amount exceeds 10,000 USD or when we perceive a higher risk associated with the customer. These precautionary steps enable us to conduct more thorough due diligence, ensuring enhanced security and regulatory compliance.

In this scenario, in addition to the standard KYC procedure, the customer must either provide proof of source of funds, or be willing to receive/send money only through bank transfers (no cash)

Ultimate KYC- Individual

We enforce our highest level of security, referred to as the “Ultimate KYC,” when transactions exceed 100,000 USD or when we identify a significant risk related to the customer. These stringent measures involve thorough due diligence, ensuring robust security and strict compliance with regulatory standards.

In this scenario, in addition to the standard KYC, the customer must provide the following:

- Proof of source of funds (must be certified)

- Proof of address (must be certified)

- Physical ID (original or certified)

In the forthcoming diagram, we outline the reasoning that governs our decision-making process to determine the suitable KYC level for corporate entities.

At our company, we apply consistent KYC levels to both corporate and individual customers. The logic behind the categorization process remains the same for all. However, for corporate customers, we require additional certified documents to verify their identity and legitimacy. This approach ensures a thorough and professional verification process, fostering trust and compliance with regulatory standards for all our valued customers. These additional documents are:

- Certificate of Incorporation

- Certificate of Incumbency

- Memorandum of Articles

- Board Resolution:

- Introducing us to the representative who is dealing with us directly, and

- Confirming that the company is authorized to buy and sell crypto assets

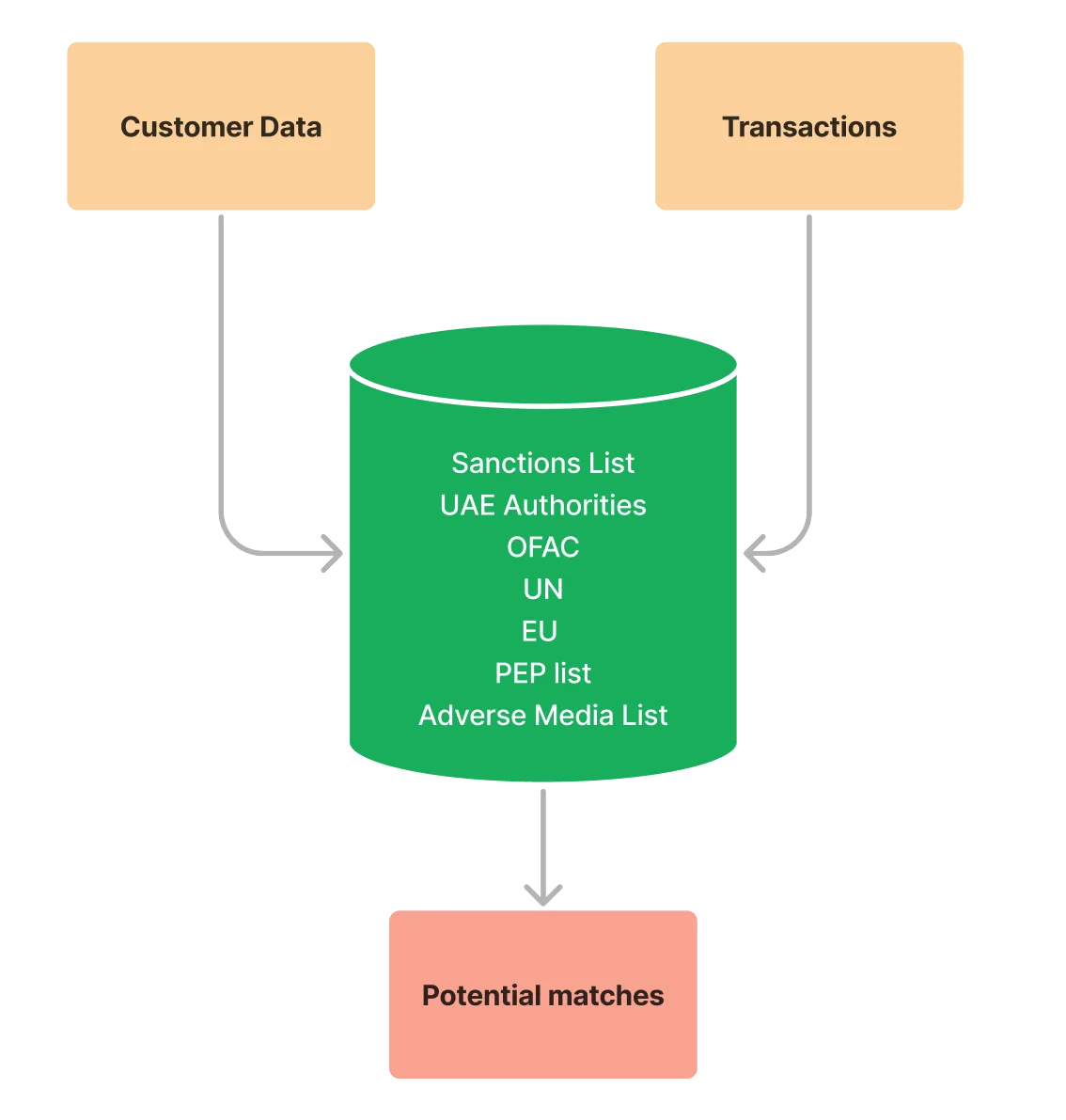

To ensure compliance with relevant sanctions imposed on individuals and entities, CryptoForce has implemented a system that screens customer names against sanctions lists issued by regulatory bodies. These bodies include the Virtual Assets Regulatory Authority (VARA, the UN Security Council (UNSC), the Office of Foreign Assets Control (OFAC), the Office of Financial Sanctions Implementation (OFSI), the European Union (EU) list, Financial Action Task Force (FAFT), and the local terrorist list issued Supreme Council for National Security. This screening process extends to all parties involved in transactions to guarantee adherence to sanctions obligations.

CryptoForce maintains a continuous process of “Transaction Monitoring” aimed at identifying transactions that exhibit unusual or potentially suspicious characteristics based on customer profiles and behavior. The initial line of defense consists of frontline staff who have the authority to promptly escalate any detected abnormal behavior or transactions using internal communication channels. Additionally, the second line of defense conducts a comprehensive review of transactions, including enhanced monitoring of customer transactions and behavior, to reinforce the effectiveness of the monitoring process.